REPORT ON THE CELSIUS NETWORK

LEGAL

DISCLAIMER

This Arkham Report on Celsius Network (the “Report”) and the content, information and opinions contained herein, is provided for educational and informational purposes only. The information provided in the Report is not intended to be a complete source of information on any particular company, investment, asset or market. The content of the Report is derived from publicly-available information and sources believed to be reliable as of the date first written. The opinions expressed in the Report are based upon the information cited herein as of the date of publication. Arkham reserves the right to amend or replace the information or opinions contained herein, in part or entirely, at any time, and undertakes no obligation to provide the reader with access to the amended information or to notify the reader thereof. Although Arkham believes the Report is substantially accurate in all material respects and does not omit to state material facts necessary to make the statements therein not misleading, all information and materials in the Report are provided on an “as is” and “as available” basis, without warranty or condition of any kind either expressed or implied. Arkham does not warrant the quality, accuracy, reliability, adequacy, or completeness of any information in the Report, and expressly disclaims any liability for errors or omissions in such information and material. In particular, Arkham shall not be liable for indirect, special, incidental, consequential, exemplary, or punitive damages of any kind, including but not limited to lost profits (regardless of whether Arkham has been notified that such loss may occur) or exposure to any third party claims by reason of any act or omission.

RISKS

You understand that you are using any and all information available in the Report at your own risk. Investing in cryptocurrency is speculative and carries a high degree of risk, including the risks of volatile market price swings or flash crashes, market manipulation, and cybersecurity risks. In addition, cryptocurrency markets and exchanges are not regulated with the same controls or customer protections available in equity, option, futures, or foreign exchange investing. Investors in cryptocurrency should conduct extensive research into the legitimacy of each individual asset, including its platform, before investing. The information contained in this Report does not take into account nor does it provide any tax, legal or investment advice or opinion regarding the specific investment objectives or financial situation of any person. You may use the Report for informational purposes and not as the sole basis for making any investment decisions. Please consult your accountant, tax advisor, stockbroker, and/or financial advisor as necessary.

SUMMARY OF FINDINGS

The cryptocurrency world is undergoing a debt crisis. Rippling defaults and market contagion threaten the solvency of some of the most prominent firms in the space. This cascade effect especially hurts asset managers relying on retail customer deposits for liquidity. Chief among these retail crypto "banks" is Celsius Network, which, since 2018, has grown into one of the largest asset managers in crypto, with almost $12 billion under management in May 2022. Facing what looks like a potential inability to meet obligations, Celsius froze customer withdrawals on June 13th. The news took the industry by storm.

Existing analysis of the Celsius crisis has been superficial, mainly relying on bits and pieces of Celsius Network announcements, anecdotal reports, and semi-public materials (e.g., investor pitch materials). Arkham Intelligence can provide a more comprehensive picture of Celsius' activity through on-chain and off-chain data and analytics. The results appear to give much deeper insight into Celsius Network's business practices, insider activity, and deployment strategies than previously reported online or in the media.

- $350 million losses by pseudonymous asset manager: Celsius appears to have entrusted corporate funds worth roughly $530 million at the time of transfer to an apparent asset manager who engaged in high-risk leveraged crypto trading strategies that resulted in $61 million of forced liquidations, for total apparent losses of $350 million when the asset manager returned capital compared to the value of the crypto assets Celsius originally sent at the time of return.

→ Arkham has identified the asset manager as the team behind investment firm Battlestar Capital / KeyFi, led by co-founder and CEO Jason Stone, pseudonymously operating as the well-known 0xB1. In October 2020, following Celsius Network’s acquisition of KeyFi, Stone held the title of Head of DeFi Staking at Celsius.

- Over $1 billion in DeFi: Despite its public emphasis on institutional lending as its source of yield, Celsius appears to have deployed over $1 billion in assets to DeFi protocols, where it lost over $100 million to hacks. After the early June crypto market crash put them at risk of liquidation, Celsius appears to have deployed roughly $750 million worth of liquid capital to these positions, potentially playing a key role in forcing them to freeze withdrawals on June 13th.

- $350 million spent buying their own token CEL: Celsius appears to have spent over $350 million purchasing their own crypto token CEL on exchanges, even though they already had billions of dollars worth of CEL in its treasury.

- $45 million in CEL sales by suspected CEO Mashinsky wallets: Blockchain addresses associated with Celsius CEO Alex Mashinsky appear to have sold $45 million of CEL throughout their lifetime, sometimes on the same exchanges where Celsius bought their own token with corporate funds, and all while Mashinsky publicly promoted CEL to Celsius customers.

Arkham was not compensated to publish this report, nor did Arkham or its leadership ever have any financial positions in CEL. Publicly illuminating the activity of large cryptocurrency institutions that have affected the lives of thousands, if not millions, makes the crypto world more robust, honest, and just.

WHAT IS CELSIUS NETWORK?

According to Celsius Network’s "About Us" page, it "provide[s] a platform of curated services that have been abandoned by big banks – things like fair yield, zero fees, and lightning quick transactions." Essentially, Celsius is a crypto retail bank offering a yield on user deposited assets. The company aims to profit on the spread between the interest it pays on deposits and the return it receives from lending those deposits out.

However, this description doesn't tell the whole story: Celsius appears to have managed a notable portion of its assets more like a hedge fund than a bank, investing deposits aggressively in the crypto markets rather than lending them out in a low-risk manner to sophisticated institutions. Because Celsius is a centralized company, much of its balance sheet exists off-chain, leaving only Celsius with the complete picture. Yet a careful analysis of the on-chain data still provides valuable insight into Celsius’ operations.

ASSETS ON CHAIN

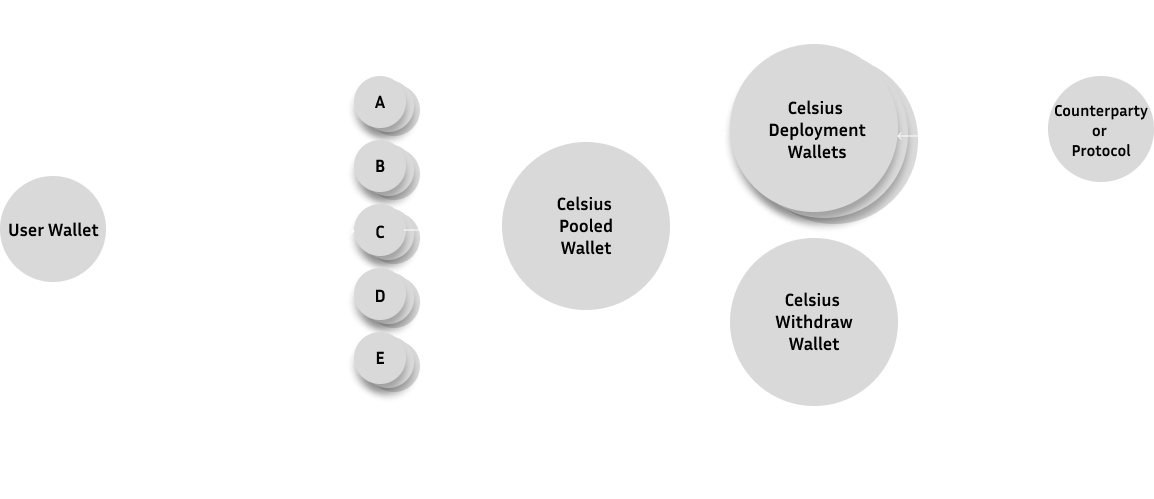

- User wallets — This is where the customer initially holds their assets before depositing them on Celsius. Services such as Metamask, Ledger, Coinbase, Binance, or others can host these wallets.

- Celsius User Specific Wallets — Celsius assigns a wallet to each customer. This wallet is where the customer deposits their crypto.

- Celsius Pooled Wallets — Celsius moves deposits from user-specific wallets to centrally pooled wallets. Celsius deploys the funds in these pooled wallets for investment strategies.

- Celsius Deployment Wallets — Celsius moves the funds from the pooled wallet to the proper wallet for each respective investment strategy.

- Celsius Withdrawal Wallets — Celsius processes user withdrawals through a separate wallet. The company sends the funds here before it sends them to the individual user.

- Counterparties or Protocols — A critical part of Celsius' business model are third parties like the institutions Celsius lends to and the DeFi protocols it utilizes.

BACKGROUND – SYNTHETIC ACCRUAL OF LIABILITIES

When a user makes a deposit on Celsius, and the funds are moved to the pooled wallet, as shown above, the user will see a balance in their Celsius Network app interface. Every week, that number will grow at the interest rate Celsius pays, giving the client the impression that they are earning “every Monday.” The customer might believe that Celsius is safeguarding these assets on their behalf. In reality, this merely represents a liability to the customer. Celsius describes this in their user terms:

Your Celsius Account is not a deposit or checking account, and Celsius does not hold any Digital Assets on your behalf. All Eligible Digital Asset balances on your Account represent Digital Assets are either loaned from you to Celsius or held by it as collateral, and therefore, owned, held and/or controlled by Celsius (under the applicable Service, as further detailed herein), and Celsius’ obligation to deliver such Digital Assets back to you upon the termination of the applicable Service.

The synthetic accrual of money owed to the user is core to understanding what happened with Celsius. On-chain data does not show Celsius' liabilities to its users. This fact makes on-chain analysis of their operations more challenging than for a DeFi protocol, for example. However, understanding how the system functions makes it possible to leverage on-chain data to form a view of Celsius operations and how things went wrong.

CELSIUS’ SOURCES OF REVENUE

One way to think about Celsius is as a supply-side and demand-side marketplace. The supply-side is where Celsius derives its costs, and the demand-side is where Celsius earns its revenues. For the business to be viable, the supply cost needs to be less than the earnings from demand.

The supply side is simple. Users lend their assets to Celsius at the rate posted on the network interface. The demand side is more complex. Celsius can be broken down into a few deployment lines or desks:

- Institutional lending – Celsius lends to institutions, exchanges, and other counterparties on terms set off-chain.

- Retail lending – Celsius allows users to borrow stablecoins against their crypto assets at an advertised interest rate.

- DeFi deployments – Celsius deploys funds into decentralized protocols that are visible on-chain. The Celsius Defi team actively allocated billions of capital to applications such as Maker, AAVE, Compound, and BadgerDAO. Celsius Network engages all kinds of strategies within this category, all with varying degrees of risk.

- Mining – Celsius publicly announced that they are expanding Bitcoin mining operations. Bitcoin mining requires the purchase of expensive mining equipment and ongoing energy costs. The mining operation denominates its expenses in dollars and returns in Bitcoin.

- Trading strategies – Though not often advertised, it is clear that Celsius would also trade with user funds. One on-chain example of corporate assets used for non-lending strategies is the stETH carry trade.

POSSIBLE SOURCES OF LOSS

Understanding Celsius' core business operations makes it possible to identify potential sources of net loss and their on-chain signatures.

- Negative carry – Lenders begin operating at a loss when the returns on their investments are less than the interest rates they promise to pay customers.

- Liability and asset volatility – Due to crypto’s volatility, coin-denominated liabilities can rapidly grow in USD value, posing additional problems for lent-out assets.

- Asset-liability denomination mismatch – Celsius Network users deposit specific crypto-assets to the platform. However, Celsius might prefer to deploy a different asset than the ones deposited. For example, if Celsius might want to swap user-deposited ETH, which it owes 5% APY on, for USDC, which it can lend out for 10% APY. In this scenario, Celsius is essentially shorting ETH. Celsius owes the client the ETH they deposited plus interest. If ETH doubles in price in a month and the user requests a withdrawal, Celsius is stuck in USDC and needs to recruit other liquidity to purchase these funds at a substantial loss.

- DeFi hacks – Engaging with and sending assets to various DeFi applications exposes Celsius to potential smart contract risk.

- Asset discount sale – This occurs when a lender acquires an asset with user funds and is then forced to sell at a discount to have the necessary liquidity to fulfill withdrawals.

- Liquidations – When on-chain loans on platforms such as Maker drop below a certain threshold, the collateralized assets are confiscated from the borrower's possession and sold on the open market. In Celsius' case, the company would have to repurchase the funds it lost that it owes its customers.

- CEL token purchases – Celsius appears to purchase CEL tokens on exchanges to fulfill interest liabilities denominated in CEL, which it offers to users at a premium compared to non CEL-denominated interest.

- Retail loan liquidation failures – When Celsius liquidates an under-collateralized retail loan, it incurs fees to facilitate the process and risks selling the assets at a discount.

- Counterparty risk – Celsius invariably exposes itself to credit risk when its loans to institutions are undercollateralized or collateralized with volatile assets.

“HIGH YIELD, LOW RISK”

Celsius Network positions itself as a wallet that enables users to "Earn" on the assets they "deposit." The "deposit" could be described as an unsecured loan from the user to the organization, and "Earn," or accrual of value to the user over time, could be described as synthetic liability accrual, meaning it is not on-chain.

Celsius attracted users by offering exceptionally high yields on deposits, such as 5% APY for Bitcoin and up to 10% for USD-pegged stablecoins – 100x the average conventional savings account interest rate of 0.1%. Celsius needs to beat these high returns through its lending and investing to make money and remain solvent. This is impracticable through conventional lending in traditional finance, where interest rates aren't high enough. Through Celsius' public materials, they claim such high yields are sustainable by the nature of the cryptocurrency market.

On the "Why Trust Celsius" section of the website, Celsius directs users to its whitepaper from 2018. This whitepaper explains that "members will be able to easily earn interest on their crypto assets the same way they earn on the savings in the bank – but with much better rates." When describing where this yield comes from, the whitepaper states, "Hedge funds, family offices and crypto funds still want to play in the world of cryptocurrency. Fortunately for us, they are willing to pay high fees to do so.”

In a video on the official Celsius Network YouTube channel titled "How Celsius earns yield," CEO Alex Mashinsky explains that Celsius earns its yield through institutional lending. According to Mashinksy, when an institution needs fast access to crypto assets for arbitrage, market making, or shorting, they borrow those assets from Celsius at a high interest rate for a short period of time. Mashinksy claims that "the key is to get a high yield at a low risk."

Building a banking business on the model of high yield at low risk can be compared to building a business on the model of buying dollars for 50 cents. It’s a perfect model, except it requires finding someone who will take the other side of the trade. If other lenders agreed that a loan was low risk then it wouldn’t be high yield, so you have to rely on systematically beating the market. This is hard to do with billions of dollars of capital at rates many times those of conventional low-risk loans, which recently have been at zero or even negative interest. In reality, despite their public emphasis on institutional lending, Celsius was chasing yield in other places that many would not characterize as low-risk.

ANALYSIS OF CELSIUS ON-CHAIN ACTIVITY

CELSIUS’ LEVERAGED DEFI POSITIONS

On-chain analysis of Celsius wallets indicates that Celsius had billions of dollars in leveraged positions on decentralized finance (DeFi) protocols that were threatened with liquidation in the June crypto market crash. In order to avoid liquidation, it appears Celsius was forced to deploy $750 million of liquid assets that could no longer be used to meet withdrawal obligations. Celsius’ decision to take these leveraged positions may have played a critical role in their decision to pause user withdrawals, swaps and transfers.

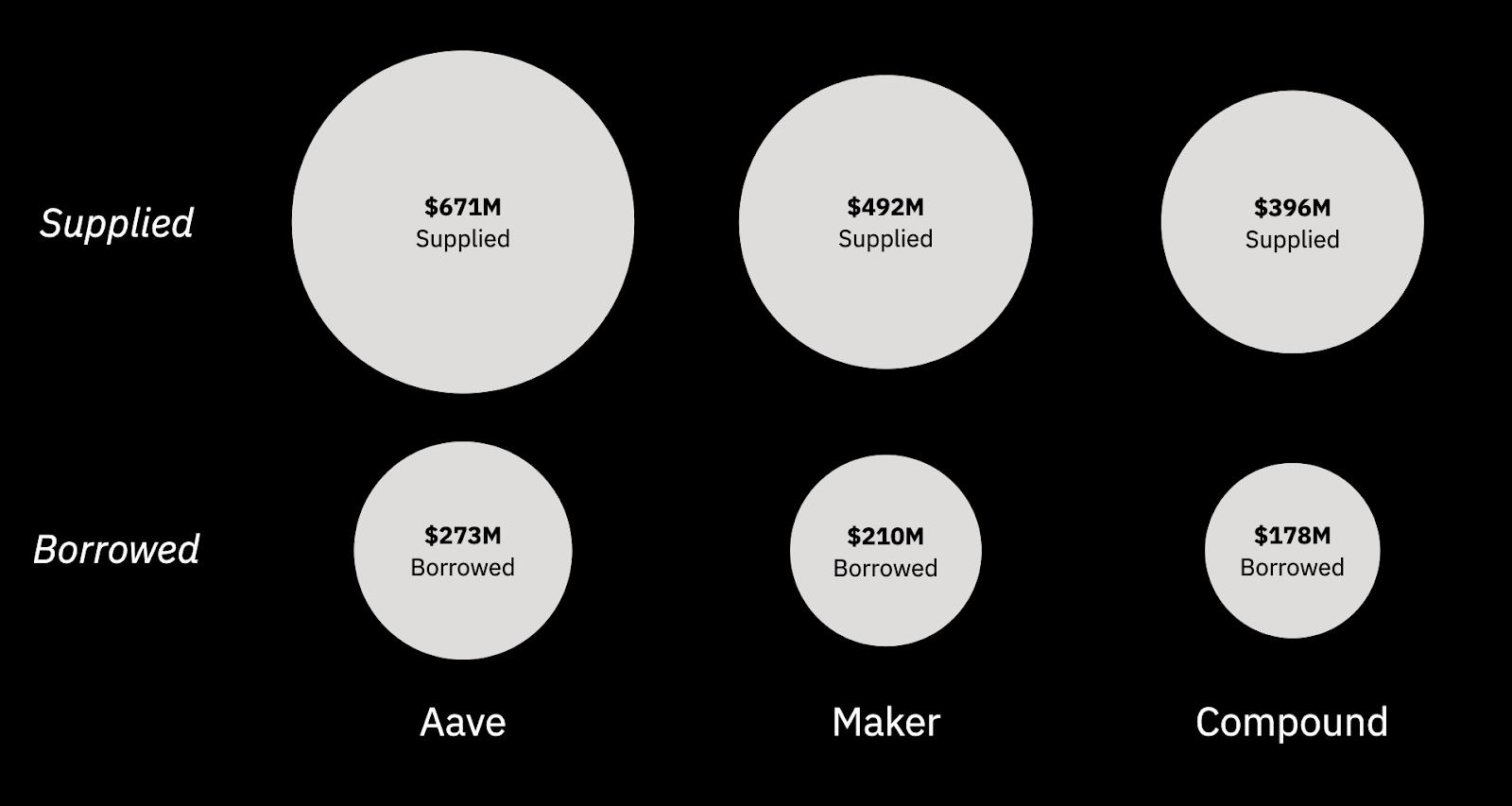

Based on Arkham’s analysis of Celsius wallets, Celsius was one of the biggest players in DeFi, accounting for a huge portion of the funds deployed to the three largest DeFi protocols, Compound, Aave, and Maker. Below are suspected Celsius DeFi positions on June 21st, 2022, eight days after freezing user accounts:

- On AAVE – 32% of stETH supplied; 17% of WBTC supplied; 6% of ETH supplied; 35% of LINK supplied; 78% of SNX supplied; 70% of xSUSHI supplied; 37% of USDC borrowed; 30% of DAI borrowed; 12% of REN borrowed.

- Celsius' cumulative positions account for 12% of the total supply and 17% of the total amount borrowed in US dollar value on AAVE.

- On Compound – 43% of WBTC supplied; 13% of ETH supplied; 57% of DAI borrowed.

- Celsius' cumulative positions account for 11% of the total supply and 20% of the total amount borrowed in US dollar value on Compound.

- On Maker – 38% of WBTC-A supply; 59% of DAI borrowed from WBTC-A pool.

- Celsius' cumulative positions account for 6% of the total supply and 3% of the total amount borrowed in US dollar value on Maker.

- ETH2 staking – 2.5% of all ETH staked.

- stETH – 10% of stETH in circulation.

A sharp decline in the price of crypto assets precipitated Celsius Network's crisis. On June 10th, 2022, Bitcoin began the day trading at around $30,000. Over the next eight days, the price fell over 40% to below $18,000. Other crypto assets experienced an even more dramatic crash during this time. On June 13th, Celsius froze all accounts. According to their official announcement, this was done “due to extreme market conditions in order to stabilize liquidity and operations while we take steps to preserve and protect assets." The market crash appears to have forced Celsius to deploy significant capital to protect their prominent DeFi positions from liquidation.

Maker allows users to borrow DAI, Maker's native stablecoin pegged to one US dollar, against various collateral options. Each loan has a maximum collateral-to-debt ratio that triggers a liquidation of the posted collateral when crossed.

On June 10th, Celsius had 17.8k WBTC of collateral in Maker and $280 million in DAI borrowed against it. The loan had a minimum collateralization ratio of 145%, meaning the position is liquidated when the collateral posted is worth less than 145% of the debt. At the time, this WBTC was worth $530 million for a 190% collateralization ratio, seemingly a comfortable cushion. But the combination of liability-asset denomination mismatch and volatility caused the strength of the position to deteriorate rapidly. In three days, the price of Bitcoin fell below Celsius' original liquidation price of $22.8k.

The fragility of Celsius' leveraged positions forced the company to use liquidity to pay down debt instead of honoring customer withdrawals. Between June 11th and June 16th, Celsius added 6.2k WBTC as collateral and paid back 53.8 million of its DAI debt, reducing its liquidation price to $13.6k per BTC. Since July 1st, they paid back another $220 million in DAI to close out the position.

AAVE rates every position on its platform with a health factor based on various risk parameters and liquidates any position with a health factor below 1.0. At the start of the market downturn, around June 10th, Celsius appears to have had $604 million of collateral against $303 million in debt on AAVE with a health factor of 1.6. On Compound, Celsius appears to have had $421 million of collateral against a $218 million debt.

During the market crash, Celsius again gathered liquid capital to shore up these liabilities, adding tens of millions of dollars worth of BTC, ETH, LINK, SNX, and BAT as collateral on AAVE and paying $30 million toward their debt. On Compound, they paid $40 million towards their debt and added over $1 million UNI as collateral.

Since June 10th Celsius has deployed $546 million in stablecoins, 7.2k BTC, 16.3k ETH, and tens of millions of dollars of other tokens to its leveraged DeFi positions. These deployments were worth roughly $750 million at the time of transactions. It is unclear how much dry powder they have left to avoid liquidation in the event of another market leg down.

DEFI HACKS THAT HURT CELSIUS

Celsius also appears to have lost over $100 million in DeFi protocol hacks. In December of 2021, the DeFi application BadgerDAO, which offers yield opportunities on WBTC, was hacked for $120 million. Celsius lost 896 WBTC in the exploit, at the time worth roughly $50 million. The way the hacker managed to exploit Celsius gives us some insight into Celsius operations. The hack appeared to exploit front-end interactions between the protocol and a user's Metamask to steal funds. This indicates that Celsius managed some of its assets in a Metamask wallet, which means no multi-party computation, no multi-sig, just a single public-key private-key pair. In an ask-me-anything interview with the Celsius community, CEO Alex Mashinsky admitted that his company lost money in BadgerDAO.

One of Celsius' DeFi yield-bearing strategies is to take Ethereum and stake it on liquid Ethereum 2.0 staking platforms. Liquid-staking allows users to enjoy Ethereum's proof-of-stake rewards without locking up assets for an extended period. Users that deposit Ethereum on these platforms receive a staked Ethereum token (stETH) in return. Liquid staking applications design each stETH to represent one Ethereum staked in the protocol and trade 1:1 with native ETH.

Celsius appears to have deposited 35K ETH on the Liquid staking platform Stakehound. On June 22, 2021, Stakehound announced they had lost the keys to all ETH staked on the platform, worth $75M million at the time. As a result, Stakehound had no ETH to return to its users, investors lost confidence, and the value of Stakehound's stETH sank to zero, losing Celsius $70 million.

Another Ethereum liquid staking platform Celsius uses is Lido Protocol. Much like Stakehound, users receive a stETH token for every ETH deposited. During recent tumultuous market conditions, Lido stETH lost its 1:1 ratio to Ether. Celsius holds over 400K stETH – worth over $400 million – on-chain. If Celsius converts a portion of its customers' ETH to stETH, an asset that now trades below the price of ETH, the company would potentially exacerbate their apparent inability to honor ETH withdrawal requests. stETH losing its peg is possibly a factor in Celsius' decision to freeze user funds.

CELSIUS BUYING CEL

Users that deposit their crypto assets with Celsius Network have two choices for how they would like to receive their yield: "In-Kind" or "In-CEL." Celsius pays users who select "In-Kind" in the same asset they deposited and users who choose "In-CEL" in CEL, Celsius' native token, at a higher APY. For example, Celsius currently advertises a 6% APY on ETH deposits paid in ETH and 7.87% APY on ETH deposits paid in CEL. Celsius explains this extra CEL in its whitepaper:

CEL are a platform utility token that is rewarded to crypto holders in the Celsius Wallet as interest on their coins. That interest is generated from fees, in CEL tokens, collected from institutional traders who use the assets pool. Celsius has a non-for-profit model where proceeds are used to cover all costs and membership growth, while most are distributed back to the members community.

These CEL tokens then get distributed back to the users lending their crypto on Celsius' website. In this model, the borrowers are the ones buying CEL. Celsius is simply collecting payment in its native token and transferring the proceeds back to its users.

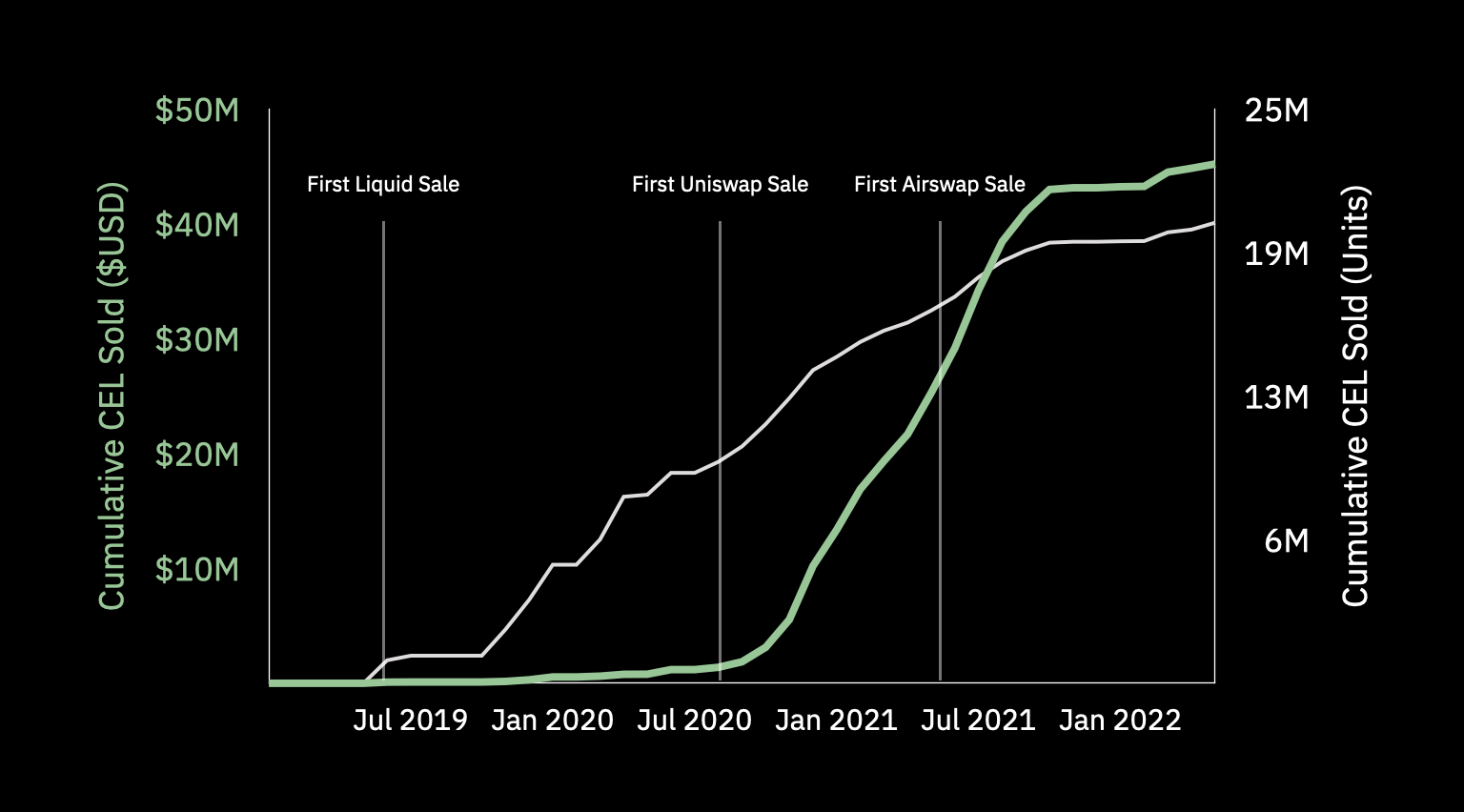

In reality it appears that, rather than redistributing in-CEL fees from lenders to users, Celsius was purchasing hundreds of millions of dollars of CEL to meet liabilities to users. On-chain analysis of Celsius’ wallets and their CEL transactions show the scale of potential CEL repurchases. Based on Arkham’s address identification and analysis, from July 2019 to March 2021 Suspected Celsius addresses withdrew over 76 million CEL from the exchange Liquid, worth $127 million at the time of withdrawal. Since December 2021, suspected Celsius addresses have also withdrawn around 82 million CEL from FTX – equivalent to 12% of the total CEL supply and worth $226 million at time of withdrawal. Since these withdrawals are not preceded by equivalent CEL deposits by Celsius, and because Celsius does not appear to use these exchanges for CEL custody, these withdrawals likely indicate CEL purchases.

Celsius purchasing its customers' in-CEL payments rather than collecting them through fees or distributing from the treasury tightens its margins as it adds another cost. On top of that, it expends capital that could otherwise be used to meet withdrawal requests, risking a liquidity crisis like the one Celsius is currently experiencing.

Even if CEL fees weren't enough to cover the in-CEL yields, Celsius doesn't need to purchase CEL to satisfy these obligations. Currently, they purport to own 335 million CEL, which amounts to around 48% of the total supply of the token, and is more than any other individual or entity owns.

One possible explanation is that Celsius purchases CEL rather than distributing it from the treasury in order to support the price of CEL by making it effectively deflationary. Paying out CEL rewards from the treasury could flood the market and cause the token price to fall. Buying CEL to pay interest has the opposite effect, likely increasing its price and thereby the wealth of CEL holders, of which Alex Mashinsky is the largest, according to Celsius, with over 45 million CEL, more than the rest of the top 5 holders combined.

THE 0xB1 STORY

CELSIUS’ RELATIONSHIP WITH 0xB1

The best illustration of Celsius' potential gaps in risk management and accounting with corporate funds is its relationship with notorious Twitter personality and Ethereum wallet address "0xB1." 0xB1 was a legendary DeFi investor during the bull run of 2020 and 2021. For background, it was the third-largest DeFi user at one point, trailing only Alameda Research and Justin Sun. The crypto community eagerly tracked 0xB1's every move, hoping to learn from one of the industry's most prominent "whales"; eventually, 0xB1 created a Twitter account to interact directly with its fans.

The DeFi giant soon became a crypto community folk hero. And yet, despite 0xB1's notoriety, it is not common knowledge where 0xB1's money originated or who exactly controlled its funds. Many crypto natives still consider 0xB1 to be a legend in the space because of the sheer amount of capital the address deployed in the market. The cryptocurrency community and the world of finance respect those who have earned their money through market acumen and accurate forecasting. With this in mind we sought to analyze 0xB1’s wallet’s activity. Cross-referencing its transaction history with Celsius wallets sheds considerable light on the otherwise pseudonymous account.

From August 2020 through April 2021, Celsius sent 0xB1 $534 million of crypto assets in 220 transactions ranging in size from $10 to $28 million. 0xB1 invested this money in various DeFi yield-bearing activities, including providing liquidity on decentralized exchanges, lending and borrowing on Compound and AAVE, and yield farming on multiple platforms. 0xB1 also purchased $6.3 million of NFTs such as Crypto Punks, Beeples, and other projects.

To contextualize the significance of the amount Celsius sent 0xB1, on December 9, 2020, Celsius announced an external audit confirming that Celsius Network had $3.3 billion in assets. By that date, Celsius had already sent $365 million of funds to 0xB1. Apparently 0xB1 had over 10% of all Celsius' assets under management in late 2020. Celsius sent 0xB1 another $180 million of their customers' crypto assets in the five months following this audit.

0xB1’S GENERAL PERFORMANCE AND SPECIFIC LIQUIDATIONS

On Thanksgiving Day, November 26, 2020, the price of ETH dropped 17%, from nearly $600 to below $500. As a result, Compound liquidated 0xB1 for 50K ETH, worth $24 million at the time. Between February 22 and 23, 2021, the price of ETH dropped almost 30%, from above $1.9K to below $1.4K. Compound liquidated 0xB1's position yet again, this time for 30K ETH, or $37 million. Ultimately, it appears 0xB1 lost $61 million of what appears to be Celsius money in liquidations.

In September 2021, 0xB1 tweeted: "We previously managed the funds held in the 0xb1 address in 2020 till May 2021, but have since escaped that relationship & no longer have any association with those funds or the organization(s) from whence they came. The team behind this Twitter has always remained the same."

0xB1 appears to have returned the majority of funds back to Celsius between September 2020 and September 2021, totalling $1.14 billion of crypto assets in that time frame. This 113% USD-denominated profit may appear to be an exceptional return on Celsius' $534 million investment. However, the performance is not nearly as impressive when denominating 0xB1's performance in the crypto assets it received from Celsius rather than in US dollars. Over the course of Celsius' relationship with 0xB1, Bitcoin increased in value from around $11,000 to around $60,000 per Bitcoin, a gain of over 400%. Ethereum, another significant asset Celsius entrusted with 0xB1, rose from almost 900% from around $400 to nearly $4000 per ETH. More plainly, had Celsius held these assets instead of sending them to 0xB1, their value would have been $1.49 billion – over $350 million more than what 0xB1 appears to have returned.

THE 0xB1 FALLOUT

Given the on-chain data and the size of these transactions, it appears customers account for a significant portion of Celsius’ funds, meaning Celsius possibly sent 0xB1 user-deposited assets that were accumulating interest. That $1.5 billion value does not factor in the interest Celsius may have pledged to pay its customers. As a result of Celsius' relationship with 0xB1, Celsius could have inadvertently ended up short of its customers' deposited assets, let alone the interest it guaranteed them. Furthermore, Celsius' business model relies on pocketing the spread between its returns and the interest it pays its users. Thus, Celsius users' account dashboards possibly informed them that they were accumulating crypto rewards that did not actually exist.

The peak US dollar value of the 0xB1 wallet was roughly $2 billion in February 2021. This is also around the same time 0xB1 began transferring funds back to Celsius. While it is clear 0xB1 sent $1.14 billion, it is unknown what happened to the rest of the funds. For example, between March 16, 2021 and April 22nd, 2021,, 0xB1 sent $39 million to an unknown Binance deposit address. Additionally, many of the NFTs are still unaccounted for. Despite spending 3,535 ETH on NFTs, 0xB1 only ever sold 76 ETH worth of said NFTs. One of the highest-priced NFT projects is CryptoPunks. 0xB1 purchased three CryptoPunks for a total of 390 ETH. Towards the end of 0xB1's relationship with Celsius, the wallet transferred these NFTs to an Ethereum wallet address starting with 0x50D. On top of this, fourteen other CryptoPunks that 0xB1 received via transfer were also send to this 0x50D address. Coincidentally, this is the same wallet that bought the NFT used as 0xB1's profile picture, Mutant Ape Yacht Club #4849. Given 0xB1's ownership of this Mutant Ape and that the Celsius-funded wallet bought the CryptoPunks, it is probable that 0xB1 transferred CryptoPunks purchased with Celsius funds to its possession.

Interestingly, on June 7, 2021, weeks after the termination of Celisus' and 0xB1's relationship, the 0xB1 wallet transferred three "Meme Ltd." NFTs to the Ethereum address "usastrong.eth." USA Strong is the business of Celsius CEO Alex Mashinsky’s wife, Krissy Mashinsky. This wallet belongs to her.

When considered holistically, a more nuanced picture of funding sources for and results of 0xB1's activity emerges. 0xB1 apparently did not earn its substantial initial principal from its own trading profits; on the contrary, Celsius appears to have handed over half a billion dollars of corporate funds to 0xB1, which then put those funds in risky DeFi positions. By the time 0xB1 returned the money to Celsius, the lending company might have been better off simply holding their corporate assets directly.

Celsius sent $534 million of its corporate crypto assets to a publicly pseudonymous group of DeFi enthusiasts to chase yields in leveraged positions. It appears Celsius did not disclose things about this relationship to the public, leaving the investing strategies utilized and the existence of the relationship in the shadows. Celsius' relationship with 0xB1 highlights how the "crypto bank" conducted its business.

THE IDENTITY OF 0xB1

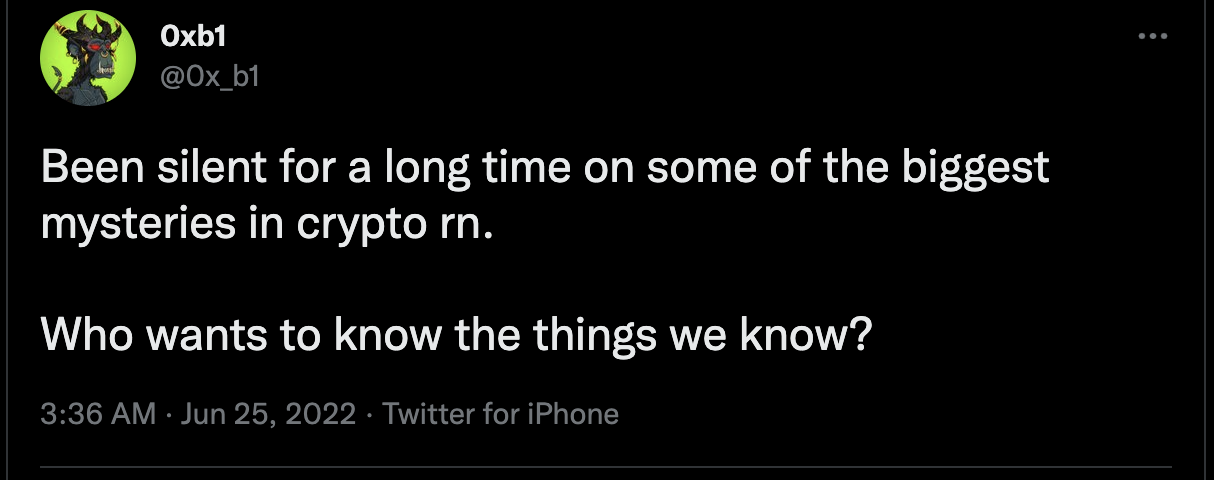

Since Celsius Network’s liquidity crisis, 0xB1 has taken to Twitter to share its perspective on the state of the crypto lending industry. While 0xB1 does not explicitly state its former relationship with Celsius, the barbs are thinly veiled:

0xB1 clearly disapproves of Celsius’ business practices. These statements also corroborate what the on-chain analysis tells us: Celsius’ management of user funds is notably different from the official story. The moral high-ground 0xB1 takes in their tweets above signals that they may understand the extent to which Celsius’ possibly mismanaged customer’s funds. The on-chain data signals that 0xB1 was at least somewhat involved. The exact legal relationship and contractual agreement between Celsius and 0xB1 remain unclear. It is also unclear where else 0xB1 may have fallen short of expectations outside of its trading performance and liquidations during one of history’s loudest roaring bull markets.

After much deliberation and internal debate, Arkham believes it is in the public interest to hear from those involved directly. When billions of dollars in ordinary people’s savings are at stake, maintaining the pseudonymity of those responsible does not constitute justice.

Arkham has identified those behind 0xB1 as the former team of crypto investment firm Battlestar Capital, later renamed KeyFi, which had a public partnership with and was later acquired by Celsius.

In an exclusive article in CoinDesk from March 2019, titled “Staking Startup Claims ‘Up to 30%’ Returns for Just Holding Crypto”, Celsius and Battlestar announced their partnership. The two firms would work together to provide “[potentially] high returns.” Adam Carver, the CEO of Battlestar Capital, is quoted in the article. Further analysis reveals Carver has also claimed to be the CEO of KeyFi – a position now held by Jason Stone. Mr. Stone has limited public associations with Celsius Network, for reasons we leave the reader to presume – but after KeyFi’s acquisition, he became the Head of DeFi Staking at Celsius, with at least one public talk in said capacity.

A further inspection into Carver and the KeyFi team reveals a crowdfunding effort by Carver’s new company, BitGreen, a DeFi protocol for climate, sustainability, and ESG activity on blockchains. On their crowdfunding page, which appears to have helped raise nearly $5 million, Carver describes himself as a co-founder of Battlestar and KeyFi, which he notes was sold to Celsius Network. Just below, Dennis Reichelt states he was also a co-founder of KeyFi, and, more importantly, a co-founder of 0xB1. Carver and Reichelt have moved on to other projects, but Stone still lists himself as the CEO of KeyFi.

Celsius customers deserve answers from the people behind Battlestar, KeyFi, and Celsius Network on the exact nature of their relationship, the risk management and accountability that was in place, and a full accounting of the funds sent to and received from 0xB1 and related entities and addresses.

SOURCES OF YIELD

THE OFFICIAL STORY

Celsius leads consumers to think that most of the yield Celsius offers its users comes from institutional securities lending. When browsing the Celsius Network website, users find multiple explanations of how their return comes from lending assets to institutions on a short-term basis. On the Celsius YouTube channel, customers find videos of the CEO of Celsius praising their institutional lending strategies and even berating the risk of DeFi yield strategies.

In a Celsius network video published on May 24th, 2022, CEO Alex Mashinsky offers his thoughts on the then-breaking Luna-Terra collapse. Mashinsky provides this advice regarding crypto yield-bearing products: "if you do not understand where the yield comes from, then you should not be in the project. If you cannot prove how the yield is earned, do not invest in the project."

The irony of this statement is that an average user of Celsius may have trouble figuring out all of the sources of their money’s yield, and their associated risks. According to what they easily see, depositing crypto in Celsius is akin to depositing money in a savings account, and the profit comes from institutional lending. Without sophisticated wallet labeling to determine which anonymous addresses belong to Celsius Network and on-chain analysis of the movement and usage of these funds, it is extremely difficult to know Celsius is hunting yield with corporate funds via leveraged positions in DeFi protocols with liquidation risk.

Alex Mashinsky admitted to using DeFi in a recent tweet after users accused his company of misleading customers on the source of yield and use of funds: "Celsius lends on DeFi when yields are high and borrows on DeFi when rates are low like now. @CelsiusNetwork is earning income from these activities." While this statement does shed some light on Celsius' business practices, there is no mention of the extent of these activities nor the half a billion dollars sent to a pseudonymous trader.

THE STATE OF THE CRYPTO LENDING INDUSTRY

The health of Celsius Network’s institutional asset loans to investment firms, BTC miners, or other parties is unclear. It is apparent that those operations do not provide enough liquidity for Celsius' DeFi positions to remain solvent while honoring their clients' withdrawal requests. In recent weeks, other crypto lending platforms have paused withdrawals or shown signs of insolvency. Voyager Digital and BlockFi took hundreds of millions of bailout dollars from crypto firms such as FTX and Alameda Research. Voyager admitted to a $675 million uncollateralized loan to now-insolvent trading firm Three Arrows Capital. In an official statement, the crypto lending firm ensured clients that they do not hold DeFi positions. BlockFi also admits its problems lie in firms defaulting on their loans and claims never to have had a DeFi position. More recently, FTX has the option to purchase BlockFi for up to $240 million – $4.56 billion less than its most recent valuation – and Voyager filed for bankruptcy.

Celsius' competitors struggle to stay in business due to their off-chain activity. Celsius utilizes institutional lending and DeFi activity to give its clients a return on their deposits. The on-chain analysis illustrates how fragile Celsius' levered DeFi positions are. Celsius has offered no comment or update regarding the health of their institutional loans. However, given recent news from Celsius' competitors, it is clear that institutional crypto lending across the board is in a tough spot. There is no reason to think Celsius' institutional lending books look much better than its DeFi positions.

On June 24, 2022, the Wall Street Journal reported that Celsius hired advisors to prepare for bankruptcy. That same day Coindesk reported that Goldman Sachs was raising $2 billion to buy Celsius' remaining assets. Both of these reports confirm the findings in Arkham's on-chain analysis: Celsius is in a position where it appears unlikely they’ll resume business as usual, barring a fortuitous bailout. Celsius is stuck hoping their over-leveraged DeFi positions do not get liquidated and their institutional loans get paid back with haste. However, if other crypto lenders are any indication, Celsius might never see repayment on their institutional loans.

The story of the Celsius Network appears to be ending sadly – with the consumer bearing the brunt of the pain. The money Celsius lost was not its own. The crypto "savings account" mismanaged the assets of consumers that thought they were making a safe deposit. What they did not know, and what on-chain analysis reveals, is that they were giving their money to something closer to a levered hedge fund.

CELSIUS CEO ALEX MASHINSKY

ASSOCIATIONS WITH WALLETS SELLING AND SWAPPING CEL

Over the past year, eight Ethereum addresses that Arkham has identified as likely belonging to Celsius CEO Alex Mashinsky have regularly sold large amounts of CEL on decentralized exchanges, totaling $44 million. At the same time that he was promoting CEL to users and denying that he was selling the token, Mashinsky appears to have been quietly selling millions of dollars of it.

Arkham identified an initial set of wallets belonging to Mashinsky by identifying particular assets he owns. For example, one address holds the NFT Mashinsky uses as his profile picture on Twitter, which requires verification of ownership. Arkham used this initial group of wallets to identify other addresses that likely belong to the same individual by analyzing address relationships such as sharing deposit addresses, frequent large transfers, and similar transaction patterns.

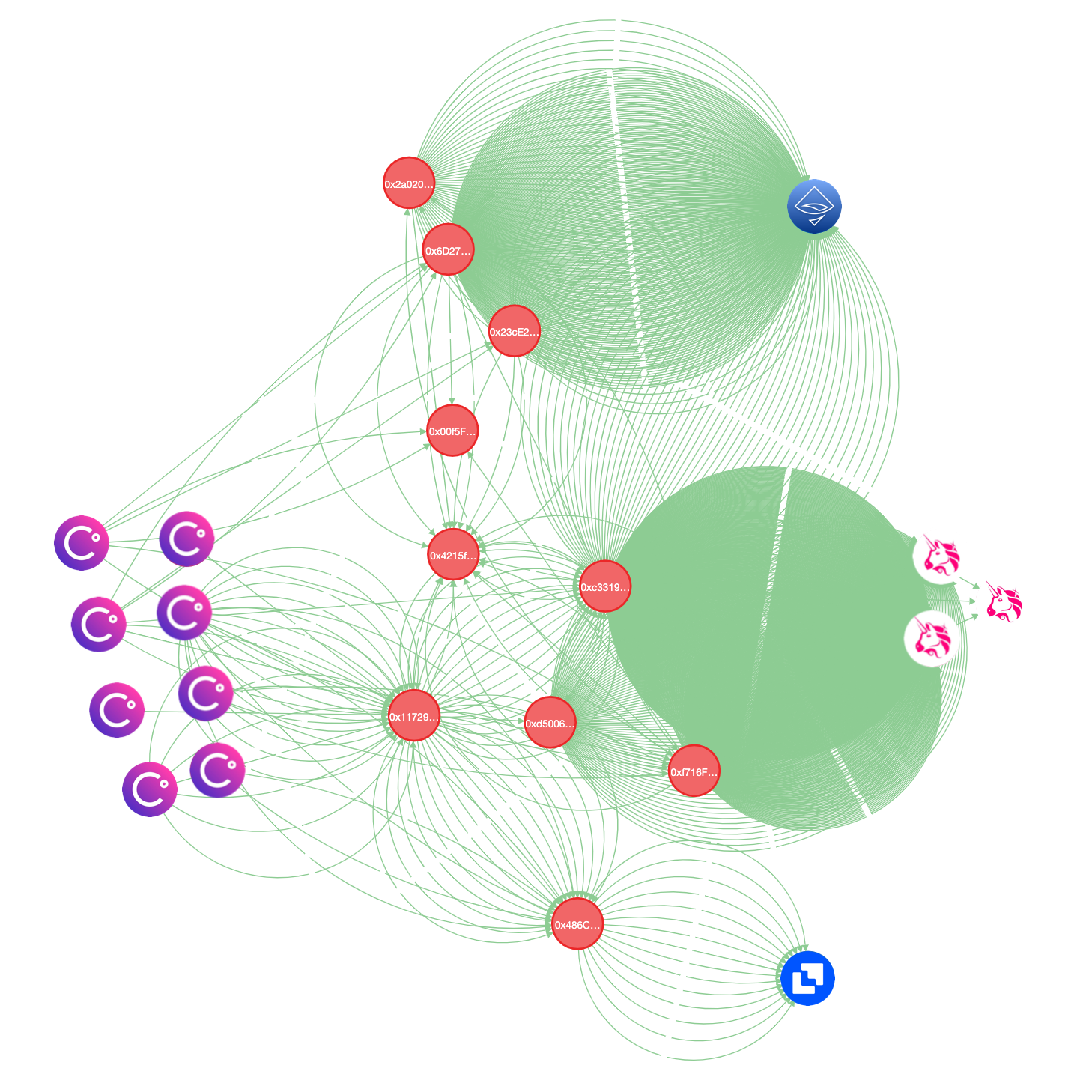

Representation of flows from Celsius to suspected Mashinsky addresses to exchanges

Most of the CEL sales from these addresses occurred on the decentralized exchanges Uniswap and Airswap. Here, Mashinsky usually swapped CEL for USDC, but in some cases for ETH or WBTC. However, one of these possible Mashinsky blockchain addresses also deposited to the centralized exchange Liquid at the same time that Celsius appears to have been purchasing large amounts of CEL on the same exchange. From June 2019 to July 2020, this suspected Mashinsky wallet deposited over 9.1 million CEL to Liquid. During the same time, Celsius appears to have purchased over 29 million CEL from Liquid. Suppose Mashinsky was selling CEL on Liquid while Celsius was buying CEL on Liquid. In that case, Celsius would have been using corporate funds on the same orderbook the CEO used to exit his position.

At the same time that he appears to have been selling the token, Mashinsky publicly promoted CEL and denied that he or other founders were selling. He also gave the impression that he was increasing his CEL holdings by publicizing CEL purchases.

On October 9th 2021, Mashinsky tweeted, “Lots to CELebrate here in #London busy week with a lot of large deals and events. It pays to #HODL.” Nine hours later on the very same day, a suspected Mashinsky wallet sold 12K CEL on Airswap for $69k in USDC. Two months later, on December 9th, he tweeted, “All @CelsiusNetwork founders have made purchases of #CEL and are not sellers of the token.” Just 5 days earlier, on Dec 4, a suspected Mashinsky address sold 11K CEL for $43K in WBTC.

Over the prior 6 months, since June 9th 2021, suspected Mashinsky wallets sold 2.8 million CEL worth over $16 million.

ASSOCIATIONS WITH SIRIN LABS

In 2017 and 2018, Mashinsky was an early supporter and official advisor to a new crypto company called Sirin Labs. On December 27, 2017, a day after the project's initial coin offering (ICO), a suspected Mashinsky address received 1,499,999 Sirin Labs tokens (SRN), all of which it sent to exchanges over the following twelve days. These transactions coincided with SRN's meteoric rise in price to a peak of $3.50, after which SRN’s price fell 71.8% to $0.98. A few weeks later, the price was $0.22. Sirin Labs published its last update on December 6, 2018, and its most recent tweet on June 6, 2021.

The founder of Sirin Labs is an Israeli businessman named Moshe Hogeg. On November 18, 2021, Israeli authorities arrested Hogeg for defrauding investors in another crypto project and sexual offenses. Around the same time Mashinsky received his allotment of SRN tokens, Celsius Network listed Hogeg as one of its earliest advisors. The Chief Financial Officer of Celsius at the time, Yaron Shalem, was also arrested on the same date in connection to Moshe Hogeg.

CONCLUSION

As of this writing, withdrawals from Celsius remain frozen, and it appears Celsius has not issued a statement guaranteeing users will recover their deposits in full. It appears some people, following Celsius and Mashinsky’s advice to “Unbank Yourself,” deposited practically everything they had onto Celsius. The stress caused by the inability to access their savings and the risk of losing everything has spilled onto public forums. In the top post of the last week on the r/Celsius subreddit, “It’s eating me up inside,” user Cheyemos writes “I can’t take it…my mind is hijacked by the Celsius situation.” Below is the post in full.

The post’s nearly 500 comments are full of other users posting similar sentiments and words of support. Some of the top comments:

“Me too my friend. I wake up in the middle of the night with panic attacks.”

“It sucks man. I've got 10x my annual income worth on Celsius. Just hoping for the best but preparing for the worst. It's all I can do.”

“I lost my lifesavings in Celsius, equivalent to about 3 years worth of income.”

These posts show the consequences of the Celsius crisis. Normal people trusted Celsius with their savings and appear very distressed that they can't access them. It is unclear whether users will access the capital they gave Celsius again or whether they will lose some or all of it -- the crisis is ongoing. These user comments show what is at stake. Moreover, these consequences underscore several foundational principles that should serve as lessons for investors and traders, including the importance of denomination when evaluating assets and liabilities and what account balances actually represent.

The sheer power of the bull run of the past eighteen months provided abundant grace for irresponsible business practices that fail in poor market conditions. These businesses appear to be reaping what they sowed. Nonetheless, plenty of institutions are well-positioned to withstand the current shocks, paving the way for a more robust system in the long run. Arkham will continue to work to advance honesty, stability, and clarity in the crypto market while empowering investors and traders with the intelligence they need to make good decisions.